Introduction

The Y-o-Y growth of soybean import in China has moved from positive to negative in 2021, as the Jan-Oct period import of soybean dropped by 4.9% against the positive growth of 8.7% recorded in 1H2021 (Tables 1 & 2). This is a surprising development as it was widely anticipated that there will be a recovery in oilmeals demand broadly expected since early this year. This opinion was shared by almost all analysts and industry members, who strongly believed that the swine farming sector is on the verge of recovery this year. As with the expected increase in soybean import and crushing activities, most oils & fats players would expect that the demand & import of palm oil in China will drop this year due to the rising output of soybean oil. But surprisingly, soybean imports dropped despite the increase in swine stocks and animal feed output.

Table 1 – Jan-Oct 2020 vs 2021 Soybean Import (Mn. MT)

| 2019 | 2020 | 2020 Jan-Oct |

2021 Jan-Oct |

Change (Vol) | Change (%) | |

|---|---|---|---|---|---|---|

| Brazil | 57.67 | 64.28 | 60.36 | 52.28 | -8.08 | -13.4% |

| USA | 17.01 | 25.89 | 14.01 | 22.59 | 8.58 | 61.2% |

| Argentina | 8.79 | 7.46 | 6.83 | 2.43 | -4.40 | -64.4% |

| Canada | 2.27 | 0.25 | 0.15 | 0.40 | 0.25 | 166.4% |

| Other | 2.84 | 2.46 | 1.87 | 1.40 | -0.47 | -25.4% |

| TOTAL | 88.58 | 100.33 | 83.22 | 79.10 | -4.12 | -4.9% |

Table 2 – Quarterly & Half-Yearly Import of Soybean (Mn. MT)

| 2019 | 2020 | 2021 | Change (Vol) | Change (%) 20-21 |

|

|---|---|---|---|---|---|

| Q1 | 16.75 | 17.79 | 21.17 | 3.38 | 19.0% |

| Q2 | 21.52 | 27.25 | 27.78 | 0.53 | 1.9% |

| Q3 | 26.32 | 29.49 | 25.04 | -4.45 | -15.1% |

| Q4 | 24.00 | 25.80 | |||

| 1H | 38.27 | 45.04 | 48.95 | 3.91 | 8.7% |

| 2H | 50.32 | 55.28 |

With the drop in soybean import and crushing activities, the import of palm oil registered a 4.3% increase in the Jan-Oct period this year against the 5.03 million MT recorded in the same period of 2020. The increase has once again proven the strong correlation between the soybean oil’s output growth against the demand/import of palm oil in China, the 2 vegetable oils that could be substituted between each other for many applications if the price is favourable.

So what were the factors that have contributed to the drop in soybean import? Will these factor(s) remain unchanged until the end of the year, and beyond?

Factors Contributing to the Drop of Soybean Import & Crushing

The sharp drop in profit margin in swine farming due to increased supplies & rising feed cost

African Swine Fever (ASF) outbreak erupted in August 2018 throughout China resulted in the number of swine to drop to a historical low in 2019 due to large-scale culling to curb the spread of the ASF virus. The spread among the swine farms mainly took place among those medium to small scale farms where most of them do not have a proper management system in place especially on waste & hygiene management. These farms account for more than 50% of the total number of swine in China. Subsequently, the sharp drop in swine numbers by approximately 40% against pre-ASF lifted the live swine prices to a historical high at approximately RMB37/kg in February 2020 and stayed above RMB35/kg throughout the year. This encouraged the swine farm to raise the number of swines especially when the ASF outbreak was well under control since early 2020.

With the rising number of live swine, the unit price of live swine experienced a gradual drop since January 2021 and experienced a sharp drop of 36% over the next 3 months until April 2021. Besides the rise in swine stock, the pockets of ASF outbreak in several regions also caused some farmers to slaughter more swine to minimize the loss if their swineherds were infected. This subsequently led to the drop of pork price due to the higher supplies in the market, and hence lowered the margin for swine farmers/farm companies.

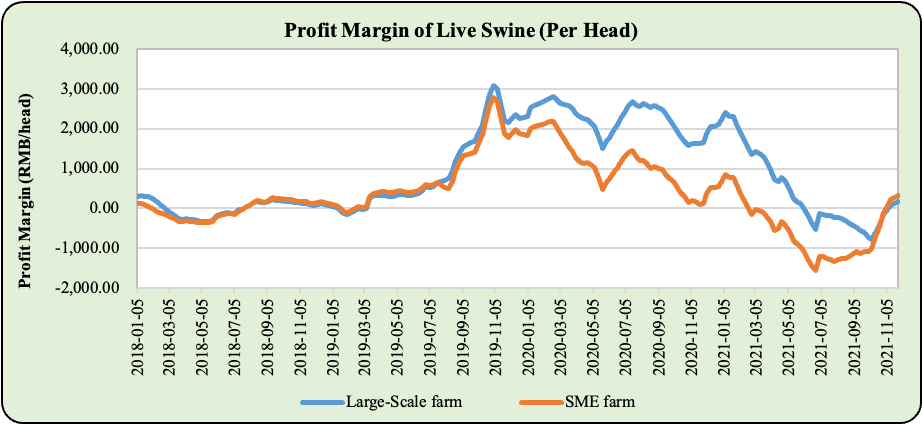

At the same time, the continuous rise in feed ingredients including soybean and corn since June 2020 has also caused the profit margin of the swine farm to drop from RMB2,400 (large-scale farm) & RMB860 (SME farms) per head in January 2021 to a negative margin since February and June 2021 for SMEs and large-scale farms respectively (Chart 1).

Chart 1 – Profit Margin of Live Swine in China

Source: FOUNDER CIFCO Futures Research Institute

This has caused many swine farms, especially those SMEs to slow down the restocking process and led to the slowdown in animal feed demand. Subsequently, this led to the drop in soybean crushing margin, and hence the slowdown of soybean demand & impacted the import.

Release of “Technical Blueprint for Reduction & Substitution of Corn and SBM Inclusion in Swine, Broiler & Layer Feed” and other policy

In recent years, China had to rely on imports to close the supply-demand gap for the supply of corn, while soybean is almost dependent fully on imports. Being a major soybean supplier to China, the US-China trade dispute, which started in 2018 led to a temporary disruption of the supplies of US soybean, which in turn affected the China soybean meal market and animal feed industry. Although the impact was minimized due to the ASF outbreak which reduced the demand for soybean meal in 2019, the Chinese government realized that the country could better utilize the locally available resources to reduce the reliance on import. Subsequently, the Animal Husbandry and Veterinary Bureau of the Ministry of Agriculture and Rural Affairs of the People’s Republic of China issued a notice on 15th March 2021, and introduced the “Technical Blueprint for Reduction & Substitution of Corn and Soybean Meal Inclusion in Swine, Broiler & Layer Feed”, as these 3 types of livestock accounted for 85% of total animal feed produced in China.

The Technical Blueprint stated that wheat, rice, cassava, rice bran, barley, and sorghum can all be used as alternative raw materials to corn, while soybean meal could be replaced with rapeseed meal, cottonseed meal, peanut meal, sunflower meal, sesame meal, corn processing by-products, etc. depending on the local resources available in different regions. Most importantly, some of the formulations recommended in the blueprint enable soybean meal to be substituted up to 100%.

Although many doubt the large-scale substitution of soybean meal recommended in the blueprint, the streamlining and utilization of local resources was not without the support from the state government, which has quietly taken place since 2019. Since 1 Jan 2019, the Chinese government has temporarily lowered the import duties of all oilmeals from 5% (MFN rate) to 0%. This temporary measure is reviewed annually and still effective. This measure allows the import of other oilmeals at a lower cost to enable it to be used as a substitute to soybean meal. Although at the end of the day, the import and substitution of soybean meal with other oilmeals is subjected to the availability and also price, this move introduced by the Chinese government is seen as a measure in cutting down the reliance on imported soybean for plant protein supplies.

Apart from this, the 4th quarter of 2020 saw the Chinese government releasing a large quantity of strategic wheat reserves into the market to ease the rising cost of corn in the country. Subsequently, the inclusion of soybean meal has been lowered as wheat contains higher protein as compared to corn and this reduces the need for soybean meal as a source of protein. According to industry sources, the inclusion rate of soybean meal in animal feed dropped from 20% to 10-14% in the first 3 quarters of 2021. This came despite the 13.8% Y-o-Y growth registered for total animal feed output for Jan-Nov 2021 period.

Finally, since the Technical Blueprint is a policy released by the state government of China, lowering the soybean meal inclusion in animal feed will somehow be implemented, but the quantum will be subjected to the availability and cost of the alternate feedstocks. Hence, we may see that the annual demand growth of soybean meal will be lower from this year onwards, indicating the slowdown of soybean meal and soybean oil output in years to come.

Impact on Palm Oil Demand

With the lower profit margin from the swine farming sector and the measures taken by the Chinese government to lower the reliance on imported soybean, the output of soybean oil in 2021 is estimated to increase marginally by 300,000 MT against last year. This is mainly due to the minimal expansion of soybean crushing activities (+1.3 million MT) forecasted for the full year of 2021. Nevertheless, the favourable import margin in 4Q 2020 has presented import opportunities to the importer/traders and led to higher import of soybean oil in 2021, which has grown by 263,900 MT Y-o-Y in the Jan-Oct period. At the same time, the favourable import margin was also seen for rapeseed oil during the same period and also led to the higher import of rapeseed oil during the same period (Table 3).

Table 3 – Import of Major Oilseeds and Oils (Thd MT)

| Jan-Oct 2020 |

Jan-Oct 2021 |

Changes (Vol.) |

Change (%) |

Jan-Dec 2020 |

|

|---|---|---|---|---|---|

| PO | 5,029.6 | 5,244.4 | 214.8 | 4.3% | 6,461.5 |

| SBO | 850.7 | 1,114.6 | 263.9 | 31.0% | 962.9 |

| RSO | 1,617.2 | 1,974.8 | 357.6 | 22.1% | 1,932.0 |

| Soybean | 83,215.5 | 79,097.8 | -4,117.7 | -4.9% | 100,327.3 |

| Rapeseed | 2,434.1 | 2,125.8 | -308.3 | -12.7% | 3,114.4 |

Source: Chinese Customs

These import growths (soybean oil and rapeseed oil) were able to offset the drop in soybean and rapeseed imports, and limited growth in crushing activities during the same period, and avoided the large supply-demand gap in the edible oil market. This explains why the import of palm oil did not surge significantly despite the demand for oils & fats being estimated to grow by 1.5 million MT in 2021 by Oil World.

Furthermore, the fact that lower global production growth of CPO in 2021 also limited the availability for export among the major producers especially Malaysia which recorded negative growth. The continuous rise in vegetable oils price including palm oil has also refrained importers and end-users from actively stocking the commodity despite the low stock level in China. Finally, the diminishing price discount advantage of palm olein against soybean oil also hinders the importers to purchase a large quantities of palm oil until this cost advantage reappears.

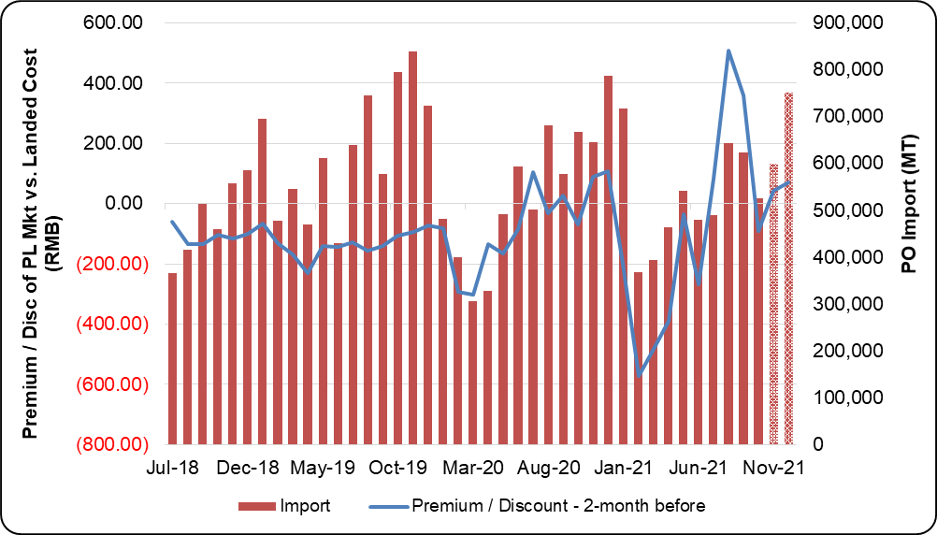

Taking into consideration the above developments and factors, and judging from the analysis on the price discount trend vs. import volume, & the historical import pattern in the last 2 months of every year (Chart 2), the total import of palm oil is estimated at 6.59 mil MT, a marginal increase of 130,000 MT or 2% from last year’s 6.46 mil MT.

Chart 2 – Import Margin of RBD PL vs. PO Import Vol.

Source: ePansun & MPOC estimates

Outlook for Soybean Meal Demand and Palm Oil Import in 2022

According to a presentation by major state-owned soybean crusher, Jiusan Group at the recent webinar held by Dalian Commodity Exchange, the total animal feed demanded in China is estimated at 400 million MT. Out of this, approximately 150 million MT of animal feed is prepared in-house by the SME farmers, while the rest which is commonly known as industrial animal feed is being produced by large-scale animal feed millers. While the industrial animal feeds are produced based on the stringent scientifically and economically calculated formula, the SME applies mainly traditional methods practiced by generations with minor adjustment in compounding the feed based on the availability of ingredients from time to time. Hence, the SME farmers tend to overuse the amount of ingredients/feed needed and this led to high wastage.

With the consolidation slowly taking place in the livestock industry, China will see more organized farms being put in place by the large-scale livestock companies in replacement of SME farms. Subsequently, the demand for industrial feed will see a gradual increase due to the move from the in-house feed. This means that the use of animal feed ingredients such as corn and soybean meal will be more efficient, cutting the total amount of feed ingredients needed to feed the same population of livestock. In another words, despite the increase in industrial animal feed output, there might be a decline or no-growth for overall demand of animal feed ingredients in years to come.

After the strong recovery in the swine sector in 2021, which also saw the increase of swine feed by 44.9% in the Jan-Nov period, the sharp drop in the profit margin of swine farming will see slower growth in the sector in 2022. This is especially for most SME farmers which are not financially strong and badly affected who will be cautious to replenish their swine stocks next year. Subsequently, the swine feed production might see stagnation in 2022 as well, as the feed production cost will remain high due to the strong commodity prices which are not expected to see any significant drop in 2022. However, with the recovery in feed production for layer hen and broiler chicken, the overall industrial animal feed production may see a marginal growth of 5%.

If the soybean meal demand from the animal feed sector increases concurrently with the feed output growth, this is will be translated into the additional 3.67 million soybean meal against what was consumed in 2021, which is estimated at 73.4 million MT. Nevertheless, as highlighted earlier, where the Chinese government is actively looking for alternate resources to replace soybean meal since the introduction of the technical blueprint, the growth of soybean meal demand might be discounted to only 2.2 million MT as forecasted by Oil World for 2021/22 season. If this additional demand is being supplemented through local crushing, the output of soybean oil will also increase by approximately 500,000 MT in 2022. This will result in the increase in the soybean import of China in 2022, but at a marginal rate.

Based on the oils & fats demand growth recorded in recent years in China, where the additional demand is ranging between 500,000 MT and 1.0 million MT annually, this will give room for a possible increase in palm oil demand and import in China 2022, provided that the global CPO output is going to recover as expected.

Prepared By: Desmond Ng

*Disclaimer: This document has been prepared based on information from sources believed to be reliable but we do not make any representations as to its accuracy. This document is for information only and the opinion expressed may be subject to change without notice and we will not accept any responsibility and shall not be held responsible for any loss or damage arising from or in respect of any use or misuse or reliance on the contents. We reserve our right to delete or edit any information on this site at any time at our absolute discretion without giving any prior notice.